This is a segment from the Forward Guidance newsletter. To read full editions, subscribe.

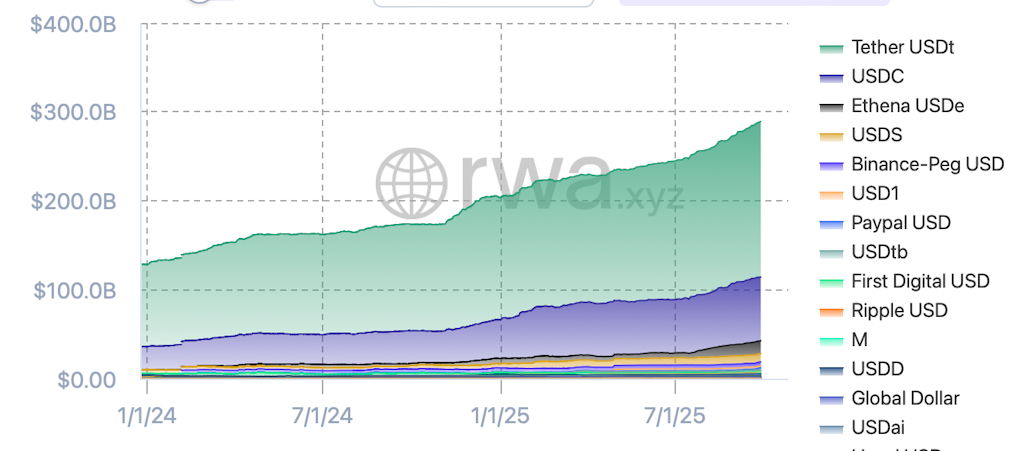

The stablecoin market is approaching the $300 billion mark as we’re seeing more signs of TradFi’s broader shift to blockchain rails.

For those keeping track at home, the roughly $290 billion stablecoin market cap is up 18% from 90 days ago and has more than doubled since the start of 2024.

We’ve seen traditional payment giants integrating stablecoins into the financial mainstream of late. Mastercard — recognizing stablecoins’ ability to bring faster, lower-cost cross-border B2B payments and simplify peer-to-peer remittances — enabled access to USDG, USDC, PYUSD and FIUSD in June. It then expanded its partnership with Circle last month.

During a Korea Blockchain Week panel last week, Mastercard’s Ashok Venkateswaran told me the stablecoin adoption snowball effect will come as institutions, banks and regulators start to act in unison.

The number of players looking more deeply at stablecoins has ramped up even in just the last six months, Venkateswaran noted. Seeing the value-add in action will be key.

“Some of these institutions have legacy systems from 100 years ago, so change is not easy,” he explained. “They want to look at it and say, ‘Well what’s the potential revenue that’s going to come out of it so that we can actually invest in the change.’”

This shift, though, is already underway.

You probably saw that the CFTC last week launched its initiative to use tokenized collateral in derivatives markets. Acting Chair Caroline Pham reiterated her belief that “collateral management is the killer app for stablecoins in markets.”

Two days later, we saw nine European banks share a plan to launch a euro-denominated stablecoin in 2026. It’s for the reasons you’ve heard before — 24/7 access to near-instant, low-cost payments and settlements. We’d expect to see these banks add services on top, such as stablecoin wallets and/or custody.

ING digital assets lead Floris Lugt said it’s “imperative” for other banks to adopt “the same standards” — aka leveraging the benefits of blockchain tech. Adapt or die, as the saying goes.

“Many banks now recognize that clinging to legacy practices could leave them vulnerable to disruption, especially as stablecoins gain relevance and the yield differential between stablecoins and near-zero interest rates on checking accounts continues to widen,” Mega Matrix markets head Colin Butler told me.

This stablecoin issuance phase follows the initial stages of institutional involvement at the custody/settlement level (i.e. BNY Mellon being a custodian for USDC reserves) and the yield/asset management level (BlackRock’s management of USDC’s short-term Treasury reserves), Butler explained.

Related, Swift said this morning that it would work with Consensys and 30 or so financial institutions to develop a shared digital ledger. It will leverage what Swift called its “unmatched resiliency, security and scalability to facilitate transactions using any form of regulated tokenized value.”

But back to the European banks for a second: That stablecoin initiative is meant to offer an alternative to the US-dominated stablecoin market, “contributing to Europe’s strategic autonomy in payments,” an ING press release noted.

Korean politician Byoungdug Min said at last week’s Origin Summit in Seoul that the country would not be buried under “the tsunami of dollar stablecoins.” Rather, there’d be work to create Korean won-backed digital money.

Maelstrom CIO Arthur Hayes told Forward Guidance’s own Felix Jauvin that he doesn’t see much of a need for certain local currency stablecoins in areas with generally good banking systems (like Asia). Demand comes instead from the underbanked who are essentially seeking a USD bank account.

Most new stablecoin projects are “zeros,” Hayes added. Here’s why he thinks so:

Where would Hayes invest in the stablecoin space? Infrastructure that allows small businesses to accept stablecoin payments and allow easy conversion to fiat, etc.

The rate at which stablecoin adoption accelerates from here will depend not only on a growing understanding of the real-world benefits, Butler said — but on overall confidence. Even with the GENIUS Act becoming law, he noted the yet-to-pass CLARITY Act would offer greater assurances for investors.

The tl;dr, as Butler puts it: “The boundary between traditional and blockchain finance is fading, and a new hybrid financial ecosystem is emerging.”

Get the news in your inbox. Explore Blockworks newsletters:

- The Breakdown: Decoding crypto and the markets. Daily.

- 0xResearch: Alpha in your inbox. Think like an analyst.

- Empire: Crypto news and analysis to start your day.

- Forward Guidance: The intersection of crypto, macro and policy.

- The Drop: Apps, games, memes and more.

- Lightspeed: All things Solana.

- Supply Shock: Bitcoin, bitcoin, bitcoin.